Indemnification clauses carrier agreements: A Practical Guide for Shippers

Understand Indemnification clauses carrier agreements, how they shift liability, and key negotiation tips to protect your business.

At its core, an indemnification clause in a carrier agreement is a legal promise where one side agrees to cover the financial losses of the other. Think of it as a financial safety net woven directly into your logistics contract, spelling out exactly who pays when something goes wrong.

What Is an Indemnification Clause

Buried deep in the dense legal text of nearly every carrier agreement is the indemnification clause—one of the most critical, and overlooked, parts of the contract. Its main job is to allocate risk. The clause assigns responsibility for specific liabilities that can pop up during shipping, like cargo damage, personal injury, or lawsuits from third parties.

Without a clear clause, a simple shipping mistake could easily spiral into a costly legal battle over who’s on the hook. By understanding how these clauses work, you can shift from just accepting a carrier’s terms to proactively managing your company's financial exposure.

Key Players in the Agreement

Every indemnification clause has two main characters:

Automate Shipping Compliance

Block orders to restricted states automatically. 3-day free trial.

Start Free Trial- The Indemnitor: This is the party promising to pay for any damages or losses. In a lot of one-sided carrier agreements, the shipper gets pushed into this role by default.

- The Indemnitee: This is the party being protected from financial harm. Carriers almost always draft agreements where they are the sole indemnitee.

Let's say a shipment gets damaged because of how the carrier handled it, but a third party decides to sue both you (the shipper) and the carrier. The indemnification clause determines whether you have to pay for the carrier’s legal defense and any damages, even if the carrier was the one at fault. This transfer of risk is what indemnification is all about.

A well-negotiated indemnification clause creates a fair distribution of risk. A poorly understood one can make your business liable for mistakes that weren't even yours, turning a routine shipment into a significant financial liability.

Why This Clause Matters for Your Business

Getting a handle on this clause isn't just a legal formality; it's a critical business function. It directly impacts your company’s financial health by deciding ahead of time who pays for accidents, regulatory fines, and lawsuits. For anyone shipping regulated goods, this is even more important, since non-compliance can trigger huge penalties and legal headaches. You can learn more about legal protection strategies for non-compliant orders to better safeguard your operations.

Managing these provisions effectively is key to long-term stability. To get a better grip on them, exploring tools like AI for indemnity clauses can offer some valuable shortcuts and insights. In the end, a clear and fair clause protects your bottom line and helps you build a healthy, predictable relationship with your shipping partners, making sure everyone knows their responsibilities long before an issue ever comes up.

The Evolution of Risk in Shipping Contracts

Indemnification clauses in carrier agreements didn’t just pop up out of nowhere. They’re the result of centuries of maritime trade, high-stakes legal battles, and a slow, grinding evolution in how businesses handle risk. Knowing this backstory gives you a serious edge in negotiations today, because it explains why the language is the way it is and how the power dynamic has shifted over the years.

Way back when, shipping contracts were incredibly one-sided, almost always favoring the carrier. The thinking was pretty simple: once your goods were on their ship, they held all the power. Shippers were often forced to accept terms that dumped nearly all the liability on them, even if the carrier was the one who made a mistake. This created a messy and expensive environment for merchants, who were often left holding the bag.

From One-Sided to Shared Responsibility

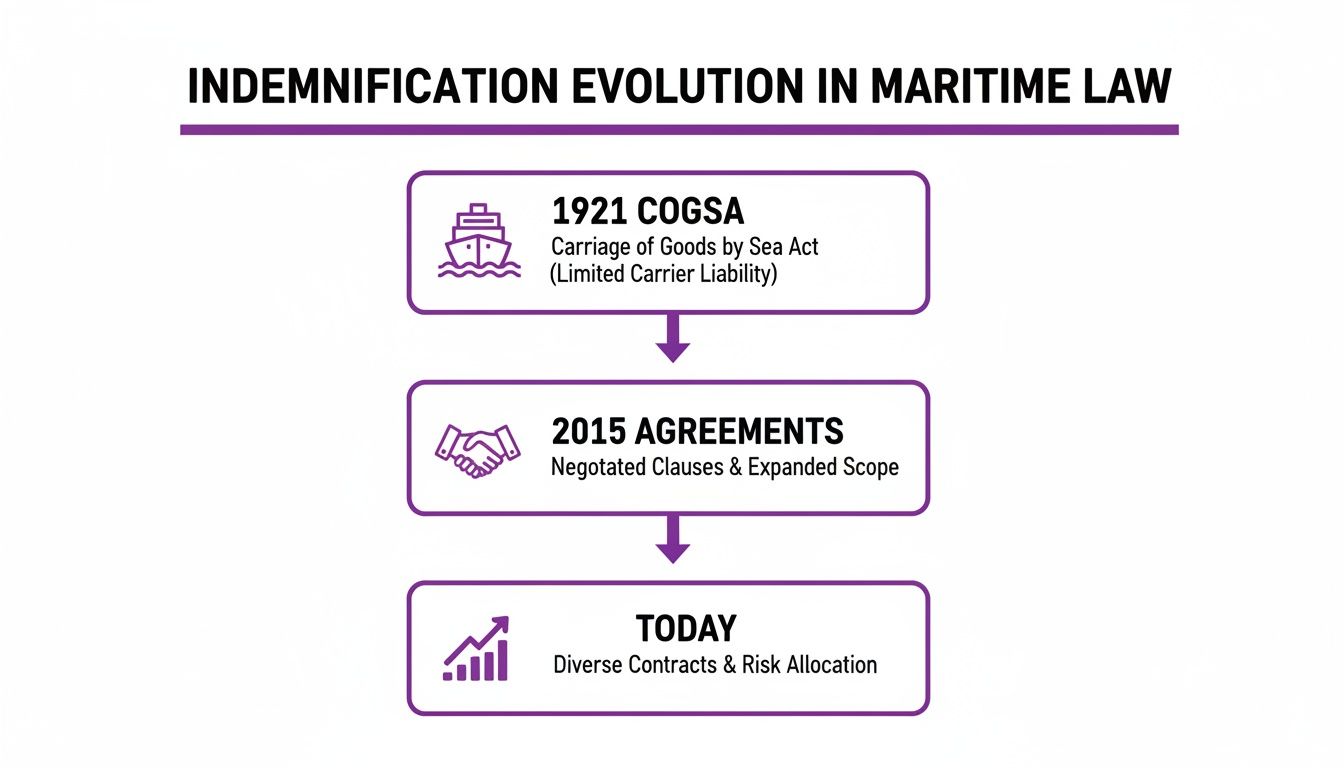

The tide started to turn with key pieces of legislation aimed at making things a bit fairer. Here in the U.S., the Carriage of Goods by Sea Act (COGSA) of 1921 was a game-changer. It set new rules for carrier liability, most famously capping it at $500 per package. This forced carriers and shippers to have a real conversation about who was responsible for what, and it still shapes how indemnification clauses are written today.

That legal shift opened the door for a more balanced way of doing things. As global trade got more complicated, smart businesses realized that shoving all the risk onto one party was just bad business. It led to endless lawsuits and broken partnerships. Over time, the industry moved toward mutual indemnification, where both the shipper and the carrier agree to cover losses caused by their own negligence. Think of it as moving from a "you break it, we both might pay" model to a much more sensible "you break it, you pay" framework. Getting this wrong can be incredibly costly, underscoring the true cost of shipping compliance violations.

The Modern State of Indemnification

That push toward shared responsibility has picked up serious steam. While indemnification clauses have always been about managing risk, the way that risk is being shared has fundamentally changed.

Free Shipping Compliance Audit

We'll review your WooCommerce store's shipping compliance for free.

A recent Deloitte survey of 500 Fortune 500 companies found that 82% of carrier agreements now include mutual indemnification. That’s a huge jump from just 45% in 2015. This shift goes hand-in-hand with a 30% drop in litigation costs, which used to average $2.1 million per dispute. You can dig deeper into these trends in contract management.

These numbers aren't just trivia; they prove that a fair, well-written agreement is a powerful business tool. It saves everyone money, time, and headaches. By understanding how we got here—from carrier-dominated contracts to a modern standard of shared liability—you have the context you need to negotiate effectively. You can push for mutual terms with confidence, knowing you’re arguing for an industry best practice that protects everyone involved.

Understanding the Three Main Types of Indemnification Clauses

When you start digging into the fine print of carrier agreements, you'll find that indemnification clauses are not a one-size-fits-all deal. The exact wording is everything. It determines precisely how much risk you, the shipper, are signing up for. Most clauses fall into one of three buckets: broad form, intermediate form, or limited form.

Knowing the difference isn't just for your legal team; it's a core business skill. Each type tilts the balance of financial responsibility, and recognizing which one you're agreeing to can be the difference between a fair partnership and a financial landmine waiting to go off. Let's unpack what each one means in the real world of shipping.

The Broad Form Clause: The Most Dangerous for Shippers

First up is the broad form indemnification clause. This is the big one—the most one-sided and perilous type for any shipper. In plain English, it makes you responsible for any and all losses, damages, or claims tied to a shipment, even if the carrier was 100% at fault.

Let that sink in. Imagine your carrier's driver blows through a red light and causes a wreck while hauling your products. With a broad form clause, you could be on the hook for the carrier's legal bills, the repairs to their truck, and any third-party injury claims. It’s like being forced to buy an insurance policy covering the carrier's own mistakes.

Because they are so incredibly lopsided, many states have passed laws making these clauses unenforceable, viewing them as contrary to public policy. But they still pop up in contracts, so you absolutely must be able to spot and reject them.

Key Takeaway: A broad form clause means you agree to pay for losses even when they are caused entirely by the other party's negligence. This is an unacceptable level of risk for any business.

The trend in legal history, as this timeline shows, has been a slow march away from these kinds of one-sided agreements and toward a more balanced approach to risk.

This evolution highlights a clear shift from the basic, often imbalanced protections of early maritime acts toward today's focus on mutual, data-driven risk management in modern carrier contracts.

The Intermediate Form Clause: A Step in the Right Direction

Next, we have the intermediate form clause. It's a bit more balanced but still packs a significant punch. This type holds you liable for losses from your own negligence and for losses stemming from the joint negligence of both you and the carrier.

Here’s the breakdown:

- If you are solely at fault (say, you packaged a fragile item poorly), you pay.

- If both you and the carrier share the blame (you used a weak box, and their team handled it roughly), you still pay for everything.

- The only scenario where you’re off the hook is if the carrier is 100% solely at fault.

It’s a huge improvement over the broad form, but the exposure is still there. If your actions contributed just 1% to an incident, you could be stuck with 100% of the costs. While more common and often legally enforceable, this clause still heavily favors the indemnitee (the party being protected, usually the carrier).

The Limited Form Clause: The Fairest Approach

Finally, we arrive at the limited form indemnification clause. This is the most equitable arrangement and what you should consider the industry standard for a fair partnership. It’s built on a simple, common-sense idea: you are only responsible for damages to the extent that they were caused by your own negligence.

This is often called a "comparative fault" provision. If something goes wrong, a court or arbitrator would figure out each party's percentage of the blame.

- If you were 40% at fault and the carrier was 60%, you’d only be responsible for covering 40% of the total damages.

- If you were 0% at fault, you pay nothing. Simple as that.

This clause creates a fair and predictable way to allocate risk. It incentivizes both you and the carrier to act responsibly, since everyone is accountable for their own actions. When negotiating indemnification clauses, pushing for a limited form clause should always be your number one goal. It's the best way to protect your business from paying for mistakes you didn't make.

Indemnification Clause Types Compared

To make this crystal clear, here’s a side-by-side look at how these clauses stack up. Notice how the risk shifts depending on the language used.

| Clause Type | Who It Protects Most | When It Applies (Example Scenario) | Typical Risk Level for a Shipper |

|---|---|---|---|

| Broad Form | The Carrier | The shipper pays for ALL losses, even if the carrier is 100% at fault (e.g., carrier's driver causes an accident). | Extreme |

| Intermediate Form | The Carrier | The shipper pays for losses from their sole negligence OR from joint negligence (e.g., poor packaging + rough handling). | High |

| Limited Form | Both Parties (Fairly) | Each party pays for their own percentage of fault (e.g., shipper pays 30% of damages if they were 30% at fault). | Low / Fair |

As you can see, the difference between "broad" and "limited" is massive. The goal in any contract negotiation is to land as close to that limited, comparative fault model as possible. It’s the only structure that truly aligns both parties toward a common goal: safe, successful shipments.

Spotting Red Flags in Your Carrier Agreements

Alright, let's move from theory to practice. This is where you actually protect your business. The legal language in indemnification clauses in carrier agreements is dense on purpose, but knowing what to look for can turn an intimidating wall of text into a clear map of your risk.

Certain phrases and even things left unsaid are giant red flags. They signal an agreement that's dangerously one-sided. Spotting these issues before you sign isn't about avoiding small headaches—it’s about preventing a financial catastrophe. Let’s break down the most common red flags so you can review any contract with confidence.

The Problematic Trio: "Defend, Indemnify, and Hold Harmless"

One of the very first things I look for is the phrase “defend, indemnify, and hold harmless.” These three words might sound like they all mean the same thing, but in the legal world, they represent three separate and escalating obligations for your business.

-

To Indemnify: This is the basic promise. You agree to pay the carrier back for any losses or damages they suffer that are covered by the clause. It's a reactive duty—you pay up after they've already paid.

-

To Hold Harmless: This goes a step further. It means you agree not to sue the carrier for any of those same losses, even if the carrier was partly at fault. It’s like putting up a shield for them against any claims you might have.

-

To Defend: This is often the most expensive and immediate threat. It forces you to step in and pay for the carrier's legal defense from the moment a claim is filed—long before anyone has even figured out who is at fault. This means hiring their lawyers and covering all court costs, right out of the gate.

Red Flag Example: "Shipper agrees to defend, indemnify, and hold harmless Carrier from and against any and all claims, liabilities, losses, and expenses..."

This simple sentence puts you on the hook for immediate, upfront legal bills that can spiral into tens of thousands of dollars before a case really even gets started. And it's not a rare problem. Data from Thomson Reuters shows that 89% of clauses separate the 'defend' and 'indemnify' duties, with those initial defense costs often making up 35% of the total payout in litigated cases. You can dig deeper into indemnification clauses in commercial contracts to see just how common this is.

Overly Broad and Vague Language

Vague language is a carrier’s best friend and a shipper’s worst enemy. You need to be on the lookout for catch-all phrases designed to expand your liability far beyond what’s reasonable.

Phrases to watch for include:

- "...arising out of or in any way related to this agreement."

- "...including but not limited to..."

- "...any and all claims, without limitation."

Language like this is a trap. The phrase "in any way related to" could mean almost anything. If a carrier's employee slips on a wet floor in their own warehouse while getting your shipment ready, they could try to argue that the accident was "related to" your agreement and demand you cover their workers' comp claim.

A More Balanced Alternative: "Shipper agrees to indemnify Carrier against claims directly caused by the Shipper's negligence or breach of this agreement."

See the difference? This revised language narrows your responsibility down to things that are clearly and directly your fault. It cuts out the ambiguity that carriers love and that leads to expensive fights over what a clause really means.

No Financial Cap on Liability

This might be the most glaring red flag of them all: an indemnification clause with no financial limit. This is the equivalent of handing the carrier a blank check drawn on your business's bank account. It exposes you to unlimited liability, a risk no company should ever accept.

An uncapped clause means a single, minor shipping mistake could theoretically trigger a multi-million dollar lawsuit that bankrupts your company.

The financial cap, often called a limitation of liability, needs to be a clear, defined number. A fair cap is usually tied to a predictable metric, making sure the potential risk is proportional to the actual business you're doing together.

Common Negotiation Points for a Liability Cap:

- The Total Contract Value: Linking the cap to the total amount of money changing hands in the agreement.

- Fees Paid Over a Period: A popular one is capping liability at the total fees you've paid the carrier over the last 12 months.

- Your Insurance Coverage Limits: Aligning the cap with the limits of your existing commercial general liability insurance policy.

An indemnification clause without a cap is a non-starter. It’s a clear signal that the carrier is trying to offload an unreasonable amount of risk onto your business. Always, always insist on a clear and fair financial limit to your obligations.

How to Negotiate Fairer Indemnification Terms

<iframe width="100%" style="aspect-ratio: 16 / 9;" src="https://www.youtube.com/embed/6H7ZQcZnusY" frameborder="0" allow="autoplay; encrypted-media" allowfullscreen></iframe>Alright, you know what to look for. Now it’s time to stop playing defense and start shaping the conversation. Negotiating indemnification clauses in carrier agreements isn’t about picking a fight; it’s about turning a one-sided document into a genuine partnership agreement.

When you do this right, you transform a huge, unknown liability into a predictable, manageable business risk. The main goal here is simple: push the clause from a unilateral (one-sided) structure to a mutual (two-sided) one.

All this means is that both you and the carrier agree to cover the losses caused by your own respective screw-ups. This isn’t some radical idea—it’s the standard for fair commercial contracts these days.

Pushing for Mutual Indemnification

You can kick off the conversation by framing the change as a win-win. A mutual clause creates a clear, predictable framework where everyone is responsible for their own actions. That alone drastically reduces the odds of ending up in a costly legal battle down the road. It builds a foundation of trust and shared responsibility from the get-go.

And you've got history on your side. The whole landscape of indemnification has shifted toward fairness, mostly because of litigation trends and smarter business practices. Before the year 2000, a whopping 83% of U.S. carrier contracts were one-sided. Fast forward to post-2010, and mutual clauses became the norm, jumping to 79%.

In fact, haggling over these clauses now takes up an average of 22% of the entire contract negotiation cycle, with 61% of that time spent arguing over liability caps.

Narrowing the Scope and Capping Liability

Once you've made the case for a mutual agreement, the next move is to rein in the scope of the clause. Vague, overly broad language is your enemy. Your mission is to narrow the clause so it only covers direct damages that result from clear negligence or a direct breach of the contract.

Here are a few key points to bring to the table:

- Strike the "Duty to Defend." Propose removing the word "defend" entirely. This is critical. It ensures you aren't stuck paying the carrier's legal bills before anyone has even figured out who's at fault.

- Insert a "Sole Negligence" Carve-Out. Add language that explicitly states you have zero obligation to indemnify the carrier for losses caused solely by their own mistakes.

- Establish a Clear Financial Cap. This is a must-have. Propose a reasonable limit on your liability. A common and fair approach is to tie the cap to a hard number, like the total fees you paid the carrier over the last 12 months or, even better, the limit of your insurance coverage. When you're negotiating, it helps to know what kind of coverage they have; for example, understanding how commercial trucking insurance impacts liability can give you leverage to propose a cap that's both fair and in line with industry standards.

Negotiation Tip: When you ask for a liability cap, connect it directly to your insurance policy. You could say something like, "Our commercial liability policy covers us up to $1 million. We propose capping our indemnification obligation at that amount to align our contractual risk with our insurable risk."

This approach isn't about dodging responsibility; it shows you're managing risk intelligently. Tying your requests to practical business realities turns the negotiation from a stuffy legal debate into a constructive business conversation. Getting the details right is crucial, and you can dive deeper into shipping insurance for high-risk products in our detailed guide.

A Practical Checklist for Reviewing Any Clause

When you’re staring at a wall of legalese, it’s easy to feel overwhelmed. But you don't need a law degree to spot a bad deal. You just need a system.

We’ve boiled down the key concepts from this guide into a straightforward checklist. Run through these questions every time a carrier agreement lands on your desk. This isn't just about ticking boxes; it's about systematically sniffing out one-sided terms and protecting your business from liabilities you never agreed to.

Think of it as your pre-flight check before signing a contract that could make or break your business.

Foundational Risk Assessment

First, let's look at the big picture. These initial questions will tell you right away if the clause is balanced or dangerously tilted in the carrier's favor.

- Is it mutual? A fair clause works both ways. Does the carrier agree to cover you for their mistakes, just as you’re expected to cover them for yours? If it’s a one-way street where only you provide the indemnity, that's a massive red flag.

- What’s the scope? Pay close attention to the wording. Does it limit your liability to claims directly caused by your negligence? Or does it use vague, all-encompassing phrases like "arising out of" or "related to"? Broad language can drag you into disputes you had nothing to do with.

- Is there a "duty to defend"? This is a big one. Does the clause force you to start paying the carrier’s legal bills the moment a claim is filed, long before anyone has determined who’s actually at fault? This can be one of the most expensive promises you can make.

Financial Exposure and Limitations

Next up, follow the money. A clause that sounds fair on the surface can still hide a financial nuke if your potential exposure is unlimited.

- Is there a liability cap? An indemnification clause without a maximum dollar amount is a blank check. The agreement must specify a limit to your potential liability. If it doesn't, that's a deal-breaker.

- Is the cap reasonable? A good liability cap is tied to something predictable, like the total amount you’ve paid the carrier in the last 12 months or the limits of your commercial insurance policy.

- Are indirect damages excluded? You want to see language that protects you from "consequential" or "indirect" damages. These are things like lost profits or business interruption costs, which can spiral into figures far beyond the actual value of the original claim.

A well-structured indemnification clause should never feel like a blank check. By ensuring liability is clearly defined, capped, and reciprocal, you transform a potential liability into a manageable business risk.

Exclusions and Carve-Outs

Finally, look for the safety hatches. These are the specific exceptions, or "carve-outs," that protect you from being held responsible for the carrier’s own blunders.

- Is the carrier's sole negligence excluded? The contract needs to state, in no uncertain terms, that you are not on the hook for losses caused 100% by the carrier's own negligence. In many states, like Indiana, forcing you to pay for a carrier’s sole negligence is against public policy and legally unenforceable.

- Are intentional acts carved out? You should never have to indemnify a carrier for damages that result from their intentional misconduct or gross negligence. If they act recklessly, that's on them, not you.

By methodically working through this checklist, you can move from feeling intimidated to feeling empowered. You’ll be able to spot the traps, understand your risk, and walk into negotiations ready to secure a fair and balanced agreement.

Indemnification Clause Review Checklist

Here's a table summarizing the key checkpoints. Use it to quickly grade any indemnification clause you encounter and decide whether the terms are good to go, require caution and negotiation, or are a definite red flag.

| Check Point | What to Look For | Status (Good / Caution / Red Flag) |

|---|---|---|

| Reciprocity | Both parties indemnify each other for their own negligence. | Good: Mutual <br> Red Flag: One-sided (shipper only) |

| Scope of Liability | Liability is limited to claims directly caused by your actions. | Good: Narrowly defined <br> Caution: Vague terms ("arising out of") |

| Duty to Defend | Obligation to pay legal fees only after fault is established. | Good: No upfront duty to defend <br> Red Flag: Duty to defend from day one |

| Liability Cap | A specific, reasonable dollar limit on your total exposure. | Good: Capped and reasonable <br> Red Flag: Uncapped / unlimited liability |

| Indirect Damages | Explicitly excludes liability for consequential or indirect losses. | Good: Excluded <br> Red Flag: Included or not mentioned |

| Sole Negligence Carve-Out | You are not liable for damages caused 100% by the carrier. | Good: Explicitly excluded <br> Red Flag: Not excluded |

| Gross Negligence Carve-Out | You are not liable for the carrier's intentional or reckless acts. | Good: Explicitly excluded <br> Red Flag: Not excluded |

Having a structured review process like this is the best defense against signing away your company’s future. It helps you catch problematic language before it becomes your problem.

Frequently Asked Questions

When you're knee-deep in a carrier agreement, a few questions about indemnification clauses pop up time and time again. Let’s get you some quick, clear answers so you can make smarter decisions when reviewing your next contract.

What Is the Difference Between Indemnification and Insurance?

Think of it like a belt and suspenders. Both are designed to hold things up and protect you, but they do it in completely different ways.

Indemnification is a direct promise between you and your carrier. It’s a two-party deal written into your contract where one side agrees to cover the other’s financial losses if something specific goes wrong.

Insurance, on the other hand, is a separate contract you buy from a third party—the insurer. You pay a premium, and they agree to cover specific, defined risks spelled out in your policy.

Key Distinction: Here’s the critical part: your insurance policy might not cover every promise you make in an indemnification clause. For example, many policies exclude liability you voluntarily take on in a contract. If you agree to a broad indemnification clause, you could be left personally on the hook for a claim you thought your insurance would handle. This is exactly why negotiating the clause itself is so vital.

Can I Just Cross Out an Unfair Indemnification Clause?

It’s tempting to grab a red pen and strike through a one-sided clause, but just crossing it out without a conversation is a risky move. Doing that can create an adversarial tone right from the start, and it could even lead to legal disputes or void the entire agreement.

A much better approach is to treat it as a negotiation, not a rejection. Instead of just deleting the language, propose a fairer alternative. Frame your suggestions as a way to build a more balanced partnership where risk is predictable for both sides. The goal is a mutual agreement that’s clearly documented in the final contract, leaving no room for ambiguity.

How Much Liability Is It Reasonable to Accept?

There’s no single magic number, but the guiding principle is simple: avoid unlimited exposure. A fair and standard approach is to cap your liability at a reasonable, predictable amount. This turns a terrifying, unknown risk into a manageable business expense.

Good starting points for this negotiation often include capping your liability at:

- The total value of the contract itself.

- The total amount you've paid the carrier over the last 12 months.

- The limits of your commercial general liability insurance policy.

Tying the cap to one of these concrete metrics anchors the risk to the actual value of your business relationship. It ensures that a single shipping mistake can't mushroom into a catastrophic financial liability that puts your company at risk.

The best way to reduce your risk from the start is to automate your shipping rules. Ship Restrict helps firearms merchants block non-compliant orders before they ever get placed, saving you time and preventing costly mistakes. Learn how Ship Restrict can protect your business.

Automate Shipping Compliance

Stop worrying about restricted states. Ship Restrict handles it automatically.

Cody Yurk

Founder and Lead Developer of ShipRestrict, helping e-commerce businesses navigate complex shipping regulations for regulated products. Ecommerce store owner turned developer.

Automate Shipping Compliance

- Block restricted states

- No more cancellations

- Set and forget

3-day free trial · Card required